New Businesses Surge but May Be Tested This Year

The American entrepreneurial spirit seems to be doing well despite high borrowing costs and consumers burdened by high prices.

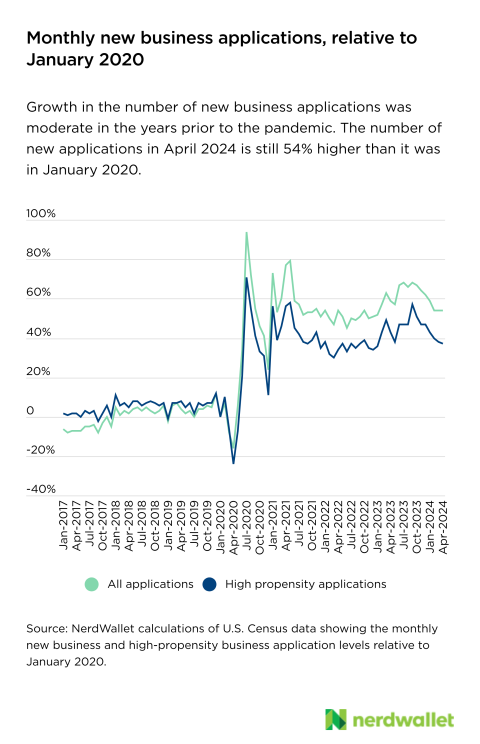

New business applications are rolling in at a monthly rate 48% higher than the 2019 average. This surge began in the immediate wake of 2020 COVID-19 lockdowns, and it continues now in both total applications and those considered “high propensity,” which are businesses most likely to result in job creation.

A flood of government funding during the pandemic, favorable programs and strong consumer demand are just a few reasons for the sustained increase in new businesses. The growth of new businesses has likely played a role in continued labor market strength, where job creation remains robust in the face of the Federal Reserve’s campaign to slow inflation through higher interest rates. However, those new businesses should craft contingency plans to weather continued high borrowing costs and softening consumer spending as 2024 wears on.

Applications surge, then remain high

In 2019, 293,000 new business applications — as measured by requests for employer identification numbers (EIN) from the IRS — were processed each month on average. This monthly measure peaked in July 2020 at 546,000. It slowed slightly before peaking again at 503,000 in May 2021 and settling to the most recent 12-month average of 455,000.

These applications weren’t solely driven by lofty fantasies conjured during lockdowns — high-propensity applications, or those deemed most likely to result in having workers on payroll, have risen and remain aloft as well.

The increases have likely been due to a combination of factors: some new entrepreneurs being among the layoffs and business closures of spring 2020; Economic Impact Payments to households helping to seed some of the startup funding; pro-small business policies; and that difficult-to-articulate shift in life priorities that occurred because of the pandemic.

Increased filings translate to increased openings

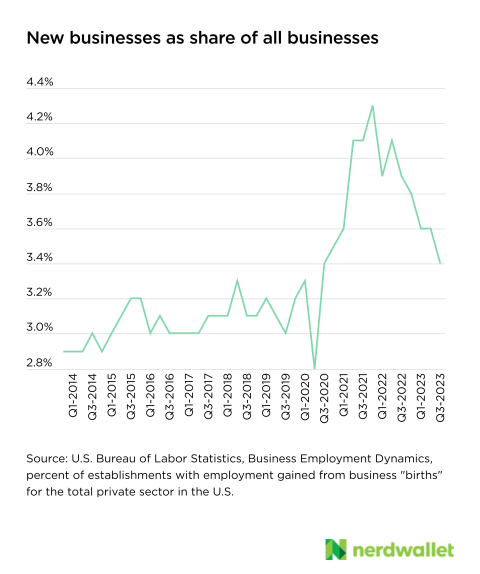

Early on, there was some debate as to whether these applications would actually result in successful business creation, i.e., would the ambitions of entrepreneurs translate to measures of success such as the hiring of employees? Thus far, the answer seems to be yes.

There is a lag between when a business files for an EIN and when it is measured as a new business or one where employees are on the payroll. In 2018-2019, these establishment “births” accounted for 3.1% of all establishments, each quarter, on average. That share grew to 4.3% in late 2021, and currently averages 3.6% over the past year.

You can also see the increased presence of new businesses when looking at business age data — the share of establishments younger than 2 years grew modestly from 15.5% in 2013 to 16.7% in 2019, before rising rapidly over the next several years. In 2023, the share of young businesses stood at 20.6%, according to Business Employment Dynamics data from the Bureau of Labor Statistics.

Funding is costly and harder to come by

These young businesses are coming of age when funding is expensive. Interest rates on new loans have roughly doubled over the past three years, according to data from the Kansas City Fed. On a loan of $100,000, for example, this difference can mean hundreds of additional dollars on a monthly payment, and tens of thousands in interest over the life of the loan.

New small business lending remained robust in the fourth quarter of 2023, according to the Kansas City Fed, but banks report lower demand for business loans in the first quarter of this year, according to the Federal Reserve. Further, in that most recent quarterly Fed survey of lenders, a moderate share of banks report tightening standards on those loans, making it more difficult for businesses to get approved for the costly funding.

What new businesses can expect in coming months

The remainder of 2024 could prove tough for new businesses. Borrowing costs will likely remain high, and consumer spending could cool.

The Federal Reserve is unlikely to begin cutting interest rates until the third or fourth quarter of the year, and it will probably begin cautiously. So new businesses shouldn’t expect any significant relief from high interest rates on loans through the end of the year.

In addition, the Fed’s efforts to quell demand-driven inflation with higher rates is likely to begin weighing more heavily on household finances in coming months. This means consumer demand for goods and services may not be as robust as it’s been for the previous few years. In fact, it’s already begun slowing, according to the most recent data from the Bureau of Economic Analysis.

New businesses are more likely to feel a negative impact from swings in consumer spending. In contrast, older businesses may have long-standing relationships with clientele — potentially greater customer loyalty — which can help buffer short-term changes in those customers’ household finances. Further, more-established businesses are likely to have more resources and greater insulation to cover periods of slower business.

Owners of new businesses can prepare for the coming months by having a game plan. Businesses that depend on discretionary spending, in particular, should plan for lean times. It’s better to be prepared and not need it than to be caught off guard. Think about where you might be able to cut expenses, consider a line of credit as an emergency fund and know where to go for help when you’re a new business owner navigating new economic experiences.